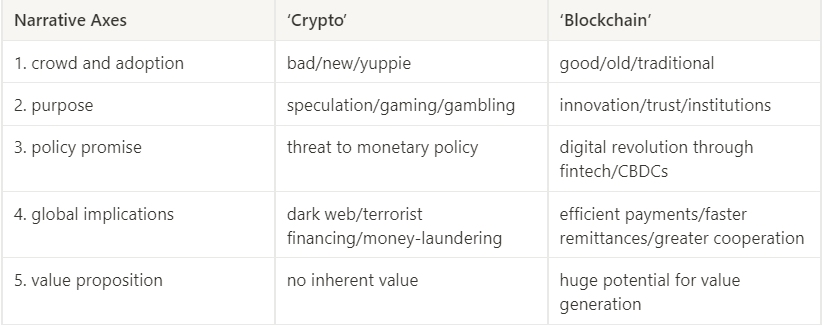

Anyone who has been following the Indian crypto space over the last year or so will probably have realised that a narrative separation is underway. ‘Good blockchain’ is being insulated from ‘bad crypto’.

While there’s no official handbook on this, one can draw up a quick primer:

A cursory glance is enough to reveal the emptiness of this approach. But we’ll do a little more in this post.

First up, the big questions – How can crypto be entirely speculative when blockchain is innovative? Why are blockchains being studied at elite universities if they have no value? Do the crimes of money-laundering and terrorist-financing not predate crypto?

Yesterday, the Hon’ble RBI Governor Shri Shaktikanta Das said this at an event:

“Every asset, every financial product has to have some underlying (value) but in the case of crypto there is no underlying [asset]… not even a tulip…and the increase in the market price of cryptos is based on make-believe. So anything without any underlying [sic], whose value is dependent entirely on make-believe, is nothing but 100 per cent speculation or to put it very bluntly, it is gambling. Since we don’t allow gambling in our country, and if you want to allow gambling, treat it as gambling and lay down the rules for gambling. But crypto is not a financial product.” (Mint, 14th Jan 2023, emphasis added)

The ‘tulip’ reference was, of course, intended to be a tongue and cheek reminder of one of the earliest financial bubbles of modernity. The sum and substance of the Hon’ble Governor’s comment is therefore quite clear: ‘all of crypto is built on hot air, stay away’.

Such a statement must be contrasted with the RBI’s CBDC push. What makes the latter such a fertile ground for innovation, we must inquire. Was the decision to move towards CBDCs a purely internal decision by the RBI, or was it necessitated by global forces?

Incidentally, the official Concept Note provides a response to this:

Private virtual currencies sit at substantial odds to the historical concept of money. They are not commodities or claims on commodities as they have no intrinsic value. The rapid mushrooming of private cryptocurrencies in the last few years has attempted to challenge the fundamental notion of money as we know it. Claiming the benefits of decentralisation, cryptocurrencies are being hailed as innovation that would usher in de-centralised finance and disrupt the traditional financial system. However, the inherent design of cryptocurrencies is more geared to bypass the established and regulated intermediation and control arrangements that play a crucial role of ensuring integrity and stability of monetary and financial eco-system.

As the custodian of monetary policy framework and with the mandate to ensure financial stability in the country, the Reserve Bank of India has been consistent in highlighting various risks related to the cryptocurrencies. These digital assets undermine India’s financial and macroeconomic stability because of their negative consequences for the financial sector. Further, a wider proliferation of cryptocurrencies has the potential to diminish monetary authorities’ potential to determine and regulate monetary policy and the monetary system of the country which could pose serious challenge to the stability of the financial system of the country.

In this context, it is the responsibility of central bank to provide its citizens with a risk free central bank digital money which will provide the users the same experience of dealing in currency in digital form, without any risks associated with private cryptocurrencies. Therefore, CBDCs will provide the public with benefits of virtual currencies while ensuring consumer protection by avoiding the damaging social and economic consequences of private virtual currencies. (RBI 2022a: pg. 7, emphases added)

There are many interrelated questions to unpack here.

- Why are cryptos not commodities? Is the US CFTC’s argument baseless?

- Is it not possible for cryptos to create legitimate ‘claims on commodities’? Is this not already happening?

- Must everything other than a CBDC be considered a ‘private’ cryptocurrency?

- Is decentralised-finance inherently evil? Or does RBI oppose it only insofar as it threatens financial stability?

- How can something ‘challenge the fundamental notion of money’ and still not have any ‘intrinsic value’?

The last of these – inherent value – takes us back to the Hon’ble Gov’s recent statement. All things considered, one must admit that it was a bold thing to say – even for a bear market.

But we needn’t be surprised. The Hon’ble Governor is known for sticking his neck out on crypto and has even assured us in the past that the next financial crisis will be born out of it. No wonder he is calling for a complete ban again. And too bad that it was struck down by the Supreme Court earlier.

Now if this were agadmator’s chess channel I would probably say:

“let me pause the video and give you a couple of seconds to find the best move…

…

…

….

And, for those of you who just wish to enjoy the show”..

Here’s the crux of this post in one sentence: the narrative binary we highlighted above has been constructed through both formal and informal mechanisms, which are in tension.

There is every reason to believe that the Hon’ble Gov’s statements reflect RBI’s true thinking on the matter. The sharper end of their sentiments could no longer be officially expressed because of the SC’s view that an outright crypto ban was a disproportional measure. Ergo, unofficial but assertive statements by the Hon’ble Gov.

And there are many reasons why this is unsustainable:

- First: none of the statements, official or unofficial, clarify why and how ‘blockchain’ and ‘crypto’ – in the RBI’s worldview – are separable. Those who know even the rudiments of Nakamoto’s white paper will be able to tell that these two ideas are joined at the hip. Blockchains have become crypto’s trademark innovation. They are the underlying value that the Hon’ble Gov is searching for. [Editor’s Note: Over the last few years, both the central and state Governments have championed blockchain-based use cases in a variety of sectors. The MeITY released a National Strategy on Blockchain in January 2021, which highlighted the potential of blockchain in real estate, governance, logistics and healthcare, among others. Many states have launched unique blockchain-based governance solutions as well. For instance, the Govt. of Maharashtra has started issuing caste certificates based on the Polygon network. Now, it’s clear that in doing so Maharashtra will need to pay Polygon’s ‘gas fee’. This shows that blockchain based governance-reforms and cryptocurrency adoption are not mutually exclusive. Since native tokens are the economic fuel of a particular blockchain, promoting one and banning the other is like legalizing toasters and banning electricity].

- Second: possibly because of this confusion, the RBI has been unable to give us any technical details about the CBDC. Is it going to be based on blockchains and DLTs? If not, is the whole thing just a payment reform? We know for a fact that it is more. The Concept Note talks at length about the possibilities of programmable money. And that is precisely the technological breakthrough Nakamoto is known for.

- Third: while economic stability is extremely important, crypto raises much bigger policy concerns – including legal and geopolitical ones. Perhaps this is why the whole CBDC game has been reduced to a pitching contest between nations – each wanting their currency to become the new world reserve. But that is impossible without innovation. And blockchains are the financial innovation of our age.

- Fourth: this is the sort of narrative confusion that leads to confusing coinages such as ‘private’ and ‘public’ cryptocurrencies. Are BTC and ETH not ‘public’? How? They are open source and allow anyone to participate. This is what makes them much more global and frictionless than fiat-currencies. And surely, it must be a bit odd to call something which is breaking jurisdictional barriers, ‘private’. Perhaps the RBI meant to refer to crypto’s pseudonymous nature. But then, cash is completely anonymous – and it doesn’t look like the RBI is planning on banning that anytime soon [ed – Dear officials, if you happen to be reading this, please don’t get ideas. We like cash.]

- Fifth: the private/public question is deeply instructive for another reason. The accepted terminology in the crypto space is ‘permissioned’ versus ‘permissionless’ blockchains. But since the CBDC Concept Note maintains a cautious distance from the latter, it may have been hesitant to adopt its native terms. Now, I’m no financial expert to tell the RBI how to run its CBDC, so I cannot say which of these models it should prefer. But if it does wish to leverage the (established and growing) network-effects of crypto then it should use them. It is entirely possible to build a centralized and permissioned e-rupee on top of them. In fact it may be possible to kill both the adoption and regulation birds with one stone.

The purpose of highlighting these points is not to suggest that the RBI is wrong about the micro and macro risks of crypto; only that it is fighting a false enemy. The problem is not all of crypto. Like every industry it has both good and bad actors. And only well-crafted regulation can help us punish one and encourage the other.

In the absence of a coherent overarching strategy on crypto – which must of course come from the Government – it seems Indian officials have been compelled to adopt a false dichotomy between bad-crypto and good-blockchain.

The RBI must surely be congratulated on its efforts to boost innovation through the e-rupee. But as the Nigerian experience shows, monetary reform is a multi-party game. At the end of the day, money is also a personal and ethical question on which people have opinions. Not to mention rights.

Over the long term, narrative confusions lead to net negative outcomes for everyone.

Let’s avoid them so we can focus on what matters – crafting regulations that can address the deeper challenges involved.

Lessons from the FTX Collapse

Lessons from the FTX Collapse The FTX collapse is a major blow to the crypto industry. It is a reminder that the industry is still in its early stages and

De-freezing bank accounts of crypto P2P traders: A Legal primer

De-freezing bank accounts of crypto P2P traders: A Legal primer Introduction Peer-to-Peer (P2P) crypto transactions executed by Indian traders have reportedly increased significantly in the last few years. These P2P transactions

FIU Registration of VDA Service Providers

FIU Registration of VDA Service Providers Introduction Regulatory landscape for cryptocurrencies i.e. virtual digital assets (VDAs) has significantly evolved in India in the last two years. Though a VDA

Are Payment gateways ‘reporting entities’ under PMLA?

Are Payment gateways 'reporting entities' under PMLA? Introduction Should a word or a phrase defined similarly in two different statutes be interpreted differently? Hon’ble Delhi High Court has answered this

An Overview of DAO Legal Wrappers

An Overview of DAO Legal Wrappers Exploring the Benefits of DAO Legal Wrappers for BusinessesBusinesses are increasingly turning to decentralized autonomous organizations (DAOs) to take advantage of the many benefits